I Have to Return Some Videotapes

I. Introduction

The 2026 release of three million pages of Department of Justice documents rewrites the history of global shadow capital (Gambino 2026). This massive repository—visitor logs, internal emails, and offshore financial contracts—exposes a continuous operational nexus between convicted sex offender Jeffrey Epstein and the highest echelons of American finance. Most crucially, the files reveal enduring, highly compartmentalized joint ventures between Epstein and Howard Lutnick, the former CEO of Cantor Fitzgerald and current United States Secretary of Commerce. For decades, Lutnick maintained a lie. He claimed he severed all contact with the disgraced financier following a 2005 townhouse visit (Kates 2026). The newly unsealed records demolish this fiction. Lutnick and Epstein executed a share purchase agreement for the advertising technology firm Adfin on December 28, 2012, using opaque limited liability companies—CVAFH I and Southern Trust Company, Inc.—to integrate their capital (Ruetenik and Kates 2026).

This financial entanglement forces a radical redirection of inquiry. We must shift focus from speculative theater to the observable mechanics of political economy. The Lutnick-Epstein alliance operates as a structural key for understanding elite impunity. It demonstrates precisely how World Trade Center legacy executives repurposed the opacity born from the September 11 systemic shocks to shield offshore wealth.

During the 2001 bond market crisis, the destruction of physical audit trails at Cantor Fitzgerald and the Pentagon granted the Securities and Exchange Commission the pretext to invoke Section 12(k) emergency waivers. These extraordinary measures suspended standard net capital requirements and customer protection rules (U.S. SEC 2001, 1–2). Financial architects seized this informational vacuum to weaponize continuous net settlement algorithms, masking $440 billion in uncollateralized debt (Fleming and Garbade 2002, 46). This systemic crisis incubated the regulatory dark pools and culture of willful blindness that elite networks subsequently used to launder billions through tier-one banks (U.S. Virgin Islands 2023, 2–3).

II. Adfin: The Lutnick-Epstein Nexus

Deception and Discovery

For over a decade, Howard Lutnick sold a story of moral revulsion. He claimed he cut ties with Jeffrey Epstein in 2005 after a single, disturbing visit to the financier's Manhattan townhouse (Ruetenik and Kates 2026). He swore he would never be in the same room as the man again. That story collapsed in 2026. When unsealed records exposed the lie, bipartisan outrage erupted. Republican Representative Thomas Massie joined Democratic Senator Adam Schiff to demand Lutnick's resignation, citing his business ties and outright fabrication as disqualifying (Greene 2026).

The Justice Department files dismantled the history Lutnick invented. Unredacted visitor logs and contracts reveal a relationship that thrived long after Epstein's 2008 conviction for procuring minors. The definitive proof is the December 28, 2012, share purchase agreement for Adfin.

The executives signed on neighboring pages. They finalized the deal just four days after Lutnick, his wife, and his children had lunch with Epstein on Little St. James (Kates 2026). The correspondence sustaining this network persisted for years. Emails show they arranged calls and meetings from 2011 until at least 2018 (Ruetenik and Kates 2026). The integration extended to high-level political fundraising. On November 3, 2015, Lutnick's assistant forwarded Epstein an invitation to a "very intimate" fundraiser for Hillary Clinton at Lutnick's home. By 2018, the relationship was familiar enough for Lutnick to instruct Epstein to deploy legal counsel against a museum expansion threatening their adjacent properties.

Structural Implications

The Adfin deal shows how World Trade Center legacy figures kept capital circulating with a sex offender. They used compartmentalized corporate vehicles to hide their joint investments. Epstein signed through Southern Trust Company, Inc., a Virgin Islands entity prosecutors identified as a funding conduit for his trafficking enterprise (U.S. Virgin Islands 2023, 7–8). Lutnick mirrored this opacity, signing for a limited liability company designated as CVAFH I. These mechanisms are verified directly in the federal files (DoJ 2012).

This arrangement proves the enduring utility of offshore havens: they bypass scrutiny; they launder the origins of co-investments; they insulate tier-one operators from the reputational contagion of their shadow partners. The systemic reality is undeniable. The elite compliance overrides and financial dark pools incubated in the early 2000s remained fully operational, facilitating the regulatory blindness necessary to protect billion-dollar enterprises.

III. Cold War Debt and the Wolfowitz Doctrine

The exhausted balance sheets of the 1980s incubated the impunity of the 2010s. Far from being a novel invention, the opacity of the Adfin deal represents a legacy of the systemic financial reset that followed the Cold War.

Debt Escalation in the Late Cold War

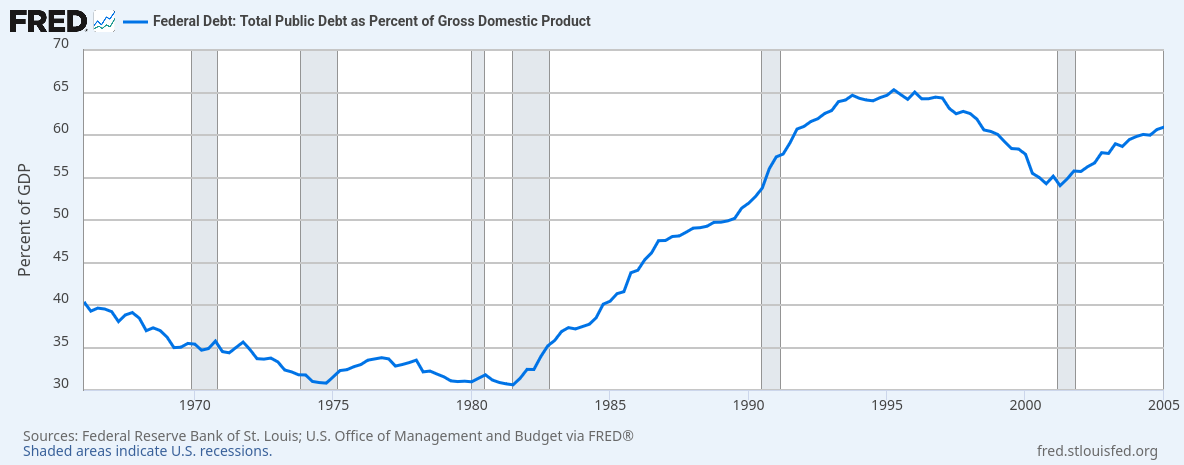

By the final decade of the Cold War, the United States was drowning in debt. While public debt relative to GDP hit a post-war low in 1974, it soon exploded. By 1980, the ratio stood at 31.81%. By the time the Berlin Wall fell in 1989, it had nearly doubled to 50.83%.

Aggressive tax cuts and massive military spending drove this surge. To maintain parity in the arms race, the U.S. tripled its national debt between 1980 and 1990, growing from approximately \$900 billion to over \$3 trillion (Dr. Econ 2000). This period defined the exhaustion of growth paradigms. The shocks of the 1970s—the collapse of Bretton Woods, the oil crises—shattered post-war stability.

The 1982 Less Developed Country (LDC) debt crisis exposed the system's fragility. Triggered by Mexico’s default on $80 billion, the crisis spread rapidly, forcing 27 countries to reschedule obligations by 1983 (FDIC 1997, 1). It posed an existential threat. By 1978, the eight largest U.S. banks held Latin American credits equal to 147% of their combined capital.

This exhausted state forced Western powers to rely increasingly on the internationalization of finance and the deregulation of credit markets to maintain operational liquidity. The transition from a production-based economy to one sustained by high-velocity debt management allowed the West to outlast the more rigid Soviet governance, but it left the global financial system burdened with massive, uncollateralized liabilities that would eventually require the systemic "resets" and regulatory overrides of the following decade.

The Wolfowitz Doctrine (Post-Cold War Militarization)

In the early 1990s, American leadership did not seek a peace dividend. They recognized that the Soviet collapse required a more aggressive, unilateral projection of power to stabilize the Western financial architecture (Scott 2007, 49–53).

The 1992 Defense Planning Guidance, known as the Wolfowitz Doctrine, codified this reality. Drafted by Under Secretary of Defense Paul Wolfowitz and overseen by Dick Cheney, the document defined a new mission: prevent the emergence of any rival superpower (Scott 2007, 162–164).

The guidance asserted a unilateral prerogative. It established the U.S. as the "world police," ready to act without the UN or NATO. It declared access to raw materials—specifically Persian Gulf oil—a core national security interest. It argued not for retrenchment, but for the "militarization of space" and high-tech weaponry to ensure no nation could challenge American hegemony (Scott 2007, 165).

President George H.W. Bush framed this as the "New World Order" on September 11, 1990. While he spoke of collective security, the reality was a strategic pivot to manage state exhaustion through global expansion (Scott 2007, 161–166). The Gulf War was the prototype. It secured energy resources and tested the militarized financialization required to sustain a debt-burdened economy. Politicians knew the U.S. had emerged from the Cold War with massive liabilities. The "world police" role justified the defense budget that supported the high-velocity trading systems—like those at Cantor Fitzgerald—recycling global capital.

This was the consensus of the deep state—the parallel security and financial structures operating outside public constraints. The transition to the New World Order bypassed the constitutional framework entirely. It prioritized the survival of the American empire over the transparency of the domestic ledger (Scott 2007, 167–170). The awareness of the need for an expanded military presence was a structural response to the reality that the global capitalist system, having outlasted its Soviet rival, now required a single, unchallenged guarantor of its debt and its energy supply. The paradox of increasing militarization at the "end of history" was, for the political class, a necessity.

IV. September 11, Cantor Fitzgerald and the Ledger Erasure

Cantor Fitzgerald: The Epicenter of Global Finance

Cantor Fitzgerald was the architectural core of the U.S. Treasury market. From floors 101 to 105 of the North Tower, the firm commanded the flow of institutional capital. Howard Lutnick joined in 1983 and rose rapidly by capitalizing on the firm's central clearing position. His "surfer's theory" defined the culture: "You see a really, really big wave. You keep surfing, keep going forward. You just don't look back" (Craig 2011). This relentless momentum drove both technological innovation and regulatory evasion.

They solidified this dominance with eSpeed. Launched in 1999, this electronic system digitized the clearance of multi-trillion-dollar government debt, transforming Cantor into a vital node of high-frequency capital. But the firm's physical location was a liability. High-altitude office space signaled dominance, but it placed the U.S. Treasury market's infrastructure on a razor's edge. In a kinetic strike, the primary clearing node would be the first to vanish.

Designed to accelerate liquidity, the system created a concentration of uncollateralized risk. The $2.3 trillion referenced by Donald Rumsfeld on September 10, 2001, quantified the "unsupported journal voucher adjustments" needed to balance incompatible Defense Department systems (U.S. Senate 2021, 4). While officially attributed to incompetence, these fabricated entries made the network unauditable. It was mathematically impossible to distinguish between broken software and the active diversion of capital. The structural fragility of Cantor Fitzgerald ensured that a systemic shock would liquidate the institutional memory required to audit the market. By September 2001, these liabilities were volatile. The calculated vulnerability of the clearinghouse transformed a potential default into a protected operational failure.

Rumsfeld issues a threat that accurate accounting of the military budget will require defense cuts (September 10th, 2001 @ CSPAN).Double Erasure: Liquidation of Oversight

The destruction of the North Tower erased this infrastructure. Six hundred and fifty-eight Cantor Fitzgerald employees died—a demographic annihilation that severed the operational continuity of the world's most critical bond brokerage (Lacker 2003, 3). This figure represents the incineration of a living community—bond traders, administrative assistants, and technology specialists whose daily rituals and networks of friendship were extinguished in a single morning.

The horror lies in its completeness. An entire social organism was trapped above the impact zone. In the calculus of the post-9/11 transition, this mass casualty event functioned as a purification ritual. The destruction of the "old" manual marketplace provided the tabula rasa for a new, opaque era of finance.

This devastation was compounded by the strike on the Pentagon's Resource Services Washington (RSW) office. The official history, Pentagon 9/11, documents this material execution. The strike on the 1st Floor of the E Ring targeted the Program and Budget and Managerial Accounting Divisions, killing 34 personnel (Goldberg et al. 2007, 28). Crucially, it devastated "Wedge 1," the newly renovated section housing the Office of Naval Intelligence (ONI). Reinforced with blast-resistant windows (Goldberg et al. 2007, 6–8), this modification paradoxically localized the destruction in the offices of the accountants investigating defense appropriations.

Official reports state that Flight 77 executed a 330-degree spiraling descent (9/11 Commission 2004, 9) to strike the western wall (Goldberg et al. 2007, 16). The attack killed 39 of 40 ONI personnel monitoring the section, decapitating the investigative body responsible for auditing military corporate transactions cleared by the targeted securities dealers (Heidner 2008, 2). These individuals constituted the specialized human infrastructure tasked with auditing the Department of Defense’s internal ledgers. These deaths occurred less than twenty-four hours after Rumsfeld announced the Pentagon's inability to track $2.3 trillion (U.S. Senate 2021, 4).

The two events hit different layers of the state. The \$2.3 trillion represented unsupported adjustments. The destruction at Cantor triggered a market clearing crisis. The Pentagon personnel were accountants mapping appropriations (Goldberg et al. 2007, 28). The \$440 billion in settlement fails at Cantor represented high-velocity trades that could not be reconciled.

This human erasure rendered digital backups inert. A ledger is only as effective as the auditors capable of contesting it. By eliminating the personnel tasked with reconciling the discrepancy, the shock ensured the untracked capital remained unaudited. Backups functioned only as a record of insolvency. The physical collapse converted a massive liability into a protected failure.

Material Reality of the Strike

The double erasure argument rests on material reality, not intent. Whether the synchronization was planned or coincidental, the outcome was the total liquidation of financial oversight.

The consequences are verifiable. Active audits ended immediately. The 34 personnel in the RSW office were the primary investigators of the \$2.3 trillion. The 658 deaths at Cantor orphaned the ledgers of 1990s militarized financial instruments. This vacuum provided the pretext for the SEC to issue Release No. 34-44791 (U.S. SEC 2001), suspending net capital rules. The resulting \$440 billion in fails allowed liabilities to be "netted out" via Continuous Net Settlement (CNS), laundering the debt into the post-9/11 order.

This double erasure functioned as a sovereign exception. It shielded the financial architecture from the public state. The destruction of auditors and brokers created a durable environment of regulatory blindness that elite networks repurposed to sustain shadow capital.

Supra-Constitutional Intervention

Beneath the macro-level preservation, survival was dictated by razor-thin margins. While the rank-and-file were eradicated, the architects remained insulated. Lutnick survived by taking his son to kindergarten. Larry Silverstein, the leaseholder, missed his breakfast at Windows on the World for a dermatologist appointment (9/11 Commission 2004, 278-315). Their survival preserved the institutional memory required to rebuild.

This continuity was reinforced by figures outside the impact zone. Lee Amaitis led Cantor's resurrection from London. Micah Green and Paul Saltzman of the Bond Market Association arranged daily calls with the Federal Reserve to prevent market seizure. Saltzman later became COO of eSpeed, illustrating the tight integration of this survival network.

Trump chopping it up with Howard Lutnick and others in the Oval Office (Feb 2026).

This contrasts with the tragedy within the towers. The collapse generated absolute physical contingency. A handful, like Brian Clark and Stanley Praimnath, survived by rejecting the fatal consensus of the crowd. Informed by fleeing victims that the stairwells were impassable, they chose to test the descent anyway, while those who ascended to the roof in hopes of rescue perished. Their survival was determined by a singular, improvised decision to push against the flow of information. The contrast between their desperate escape and the executive class's insulation underscores a structural reality: systemic shocks devastate the human foundations of an institution, while power networks survive to override regulations in the fog of war.

The horror provided a moral safe harbor. Elite networks weaponized the trauma to bypass gridlock. The shock served as a shield, allowing leadership to collaborate with federal authorities to clear massive liabilities. The $440 billion in fails represented a structural crisis. Architects leveraged the destruction to mask aging bonds within the backlog of event-related failures.

They used CNS algorithms to fold uncollateralized liabilities into legitimate trades (Fleming and Garbade 2002, 46). CNS permits netting through novation, where the clearinghouse becomes the central counterparty (Ingber 2017, 38). In the chaos, phantom bonds were netted against real transactions, laundering the debt.

The SEC's Emergency Order (Release No. 44791) codified this reset (U.S. SEC 2001, 1–2). This waiver of net capital rules created a five-day regulatory dark pool. It allowed institutions to trade without proving they possessed the underlying capital, purging phantom obligations from the global balance sheet.

This was a supra-constitutional intervention. As Peter Dale Scott argues in The Road to 9/11, it was an override of the public state by deep state actors (Scott 2007, 28–30). The emergency measures allowed the deep state to resolve historical liabilities in secrecy, prioritizing the banking architecture over bond obligations. The catastrophe incubated the dark pools used to launder billions, converting loss of life into a mechanism for permanent financial opacity.

V. Zero-Risk Arbitrage

The destruction of Cantor Fitzgerald's blind-basis broker records severed the data links required for the Government Securities Clearing Corporation to compare trades (Lacker 2003, 6). Uncompared transactions fell outside the netting process. Without advisory messages, the clearinghouse recorded $266 billion in failed transactions by the close of September 11 (Fleming and Garbade 2002, 46).

To mitigate the risk of unmatched transactions, the clearinghouse invoked emergency overrides. On the evening of September 11, it administratively created and compared 2,178 broker trades valued at over $71 billion based solely on unverified, one-sided data (Ingber 2017, 48). By forcing these asymmetric submissions into the net, the clearinghouse deployed blind-basis novation to mask the compounding interdealer fails within the opaque centralized ledger (Fleming and Garbade 2002, 45–46). In plain English, the clearinghouse mixed valid trades with broken ones, making it impossible to distinguish solvent debts from bad ones. The blindness of the ledger reflected the physical blindness of a market that had lost its architects.

This informational vacuum caused interdealer settlement fails to compound geometrically. As brokers struggled to reconcile blinded trades without physical ledgers, aggregate fails across the network skyrocketed to $440 billion by September 12.

To prevent systemic insolvency, the SEC invoked Section 12(k) emergency powers. This intervention altered the physical laws of the market. The SEC suspended the uniform net capital rule (Rule 15c3-1) and the customer protection reserve requirements (Rule 15c3-3) (U.S. SEC 2001, 4). Rule 15c3-1 mandates that broker-dealers maintain liquid reserves to satisfy claims. Rule 15c3-3 requires the segregation of customer funds. The September 14 order eviscerated this framework. By exempting broker-dealers from calculating charges arising from failed transactions, the regulatory state legalized the indefinite retention of investor cash without the delivery of the underlying security.

Uniform Commercial Code Article 8 provided the statutory basis for this transmutation. It allowed for the creation of a securities entitlement—a legal IOU representing a claim to ownership—while the failing broker-dealer retained the buyer's cash unencumbered by reserve strictures. The code prioritizes absolute account finality, dictating that an investor acquires a security entitlement "regardless of whether or not the intermediary has obtained the corresponding financial asset" (FMLC 2004, 13). This birthed an influx of phantom shares—digital apparitions that exist on statements but do not correspond to outstanding stock. These un-delivered shares dilute the voting power and equity value of the targeted corporation (ALI and NCCUSL 1994, Part 5), destroying market integrity and initiating a transfer of wealth to illegal short sellers (Shapiro 2003, 2). This provided the blueprint for the offshore opacity Epstein and Lutnick would utilize in the Adfin deal—a system where ownership is a legal fiction divorced from physical reality.

This controlled environment manifested in the disintegration of the Bank of New York's (BoNY) settlement infrastructure. Physically crippled, BoNY became a black hole for transaction data (Lacker 2003, 6-7). This paralysis triggered a systemic liquidity crisis that forced the Federal Reserve to flood the banking sector with over \$100 billion in emergency funds by September 12 (McAndrews and Potter 2002, 60-65). The "bubble" was a massive accumulation of settlement fails; system-wide failures to deliver securities skyrocketed from \$1.7 billion per day to \$190 billion by September 19 (Fleming and Garbade 2002, 45). The emergency waivers established a sanctioned dark pool to process this backlog.

The Federal Reserve's intervention eliminated the market friction preventing infinite settlement failure. As the central bank slashed the federal funds rate from 3.5 percent to 3.0 percent on September 17, the "specials rate" required to borrow the benchmark ten-year Treasury note collapsed to zero (Fleming and Garbade 2002, 47). This shift birthed zero-risk arbitrage. When the cost of borrowing a liquid security drops to zero, market actors lose the incentive to fulfill settlement obligations (Schneider 2025, 10). Failing to deliver became more profitable than executing the trade.

Sophisticated participants capitalized on this by lending securities on term repurchase agreements and intentionally defaulting on the starting leg, generating risk-free yield from a paralyzed architecture (Fleming and Garbade 2002, 47). Put simply, institutions could "sell" securities they didn't have, collect the cash, and earn interest without ever delivering the bond. Transaction data confirms that options market makers elected to fail to deliver rather than accept negative borrowing rebate rates (Evans et al. 2006, 3-4). This was the moment Lutnick's surfer's theory—relentless forward momentum regardless of the wreckage—became the dominant physics of the financial system.

This zero-risk arbitrage environment was a deliberate pivot by institutional players acting with foreknowledge (Zarembka 2008, 67–68). To alleviate the artificial scarcity, the regulatory apparatus deployed a \$6 billion snap reopening of the 10-year note on October 4, 2001 (Fleming and Garbade 2002, 48). This artificial injection stood as the only mechanism capable of resolving the gridlock. The result confirmed the thesis: the sudden influx caused the specials rate to rise above zero, restoring the cost of failure. Daily average fails plummeted from \$142 billion to \$63 billion the following week (Fleming and Garbade 2002, 49), proving the crisis was driven by rational arbitrage rather than dysfunction.

The financial irregularities of September 2001 represent a macro-financial pivot. Elevating the macroeconomic implications reveals a covert timeline; the destruction of physical ledgers provided the opacity required for the off-book clearing of massive, clandestine 10-year Treasury notes utilized to fund the 1991 Gulf War debt and illicit Cold War-era intelligence operations, frequently referred to as "Project Hammer" (Heidner 2008, 5). The crisis proved to shadow capital networks that massive uncollateralized liabilities could be perpetually sustained under the aegis of market continuity.

This continuity was foreshadowed by anomalous market signals. In the days preceding the attacks, a massive spike in put options was recorded for United and American Airlines (Poteshman 2006, 1703). Abnormal long put volume reveals unusually high levels of activity, consistent with informed investors trading on advance knowledge (Poteshman 2006, 1725). These deviations suggest a landscape of asymmetric information where specific actors possessed a systemic awareness of impending volatility.

Regulatory authorities weaponized the trauma to justify the permanent institutionalization of pre-existing policy objectives. They transformed the temporary suspension of delivery obligations into a permanent structural feature. The ensuing continuous net settlement algorithms socialized the fails across the network, incubating the architecture of systemic naked short selling that elite syndicates would repurpose for decades. This reality is evidenced by the fact that an average of $33 billion in benchmark U.S. Treasury contracts continues to fail to settle every single day (Schneider 2025, 4).

VI. Shadow Capital Architecture: Epstein and the WTC Legacy

The consolidation of global shadow capital requires a sophisticated vanguard. JPMorgan Chase was the primary banking engine for Jeffrey Epstein's transnational trafficking enterprise, integrating illicit offshore funds into the legitimate system. The aggressive, risk-tolerant culture of World Trade Center legacy firms—specifically Salomon Smith Barney in WTC 7—permeated JPMorgan. This lineage traces to Sandy Weill, the architect of Citigroup. Jamie Dimon, Weill's protégé at Smith Barney, carried this philosophy—capital capture over regulatory fidelity—directly to JPMorgan Chase (Langley 2003, ch. 3). This culture neutralized compliance to accommodate elite perpetrators.

For over a decade, JPMorgan deliberately bypassed Anti-Money Laundering protocols to process an estimated $1.3 billion for the Epstein enterprise (U.S. Virgin Islands 2023, 16–18). The bank maintained fifty-five compartmentalized accounts for Epstein's shell companies, facilitating suspicious cash withdrawals and wire transfers to recruiters and victims (2023, p. 10). Executives like Jes Staley—who visited Epstein's victim stash houses—shielded the network from scrutiny, prioritizing lucrative client referrals over legal compliance (2023, pp. 12–14).

The institution delayed filing Suspicious Activity Reports until after Epstein's death in 2019, a strategy of willful blindness (U.S. Virgin Islands 2023, 21–22). This blindness is insulated by Article 8's "protected acquirer" rule, which shields tier-one institutions from adverse claims so long as they "did not act in collusion," creating an insurmountable evidentiary bar (FMLC 2004, 14).

The collapse of WTC 7 provided a parallel erasure for the investment banking arm. The destruction annihilated the offices of Salomon Smith Barney and the files for 3,000 to 4,000 active SEC cases (Heidner 2008, 46). These lost archives targeted "yield burning" fraud and municipal bond overcharging, neutralizing probes into the firm's predatory practices and insulating executives who migrated to JPMorgan. This complicity extended to insurance giants. Marsh & McLennan, in the North Tower impact zone, maintained deep "elite interlocks" with Epstein's financier, Leon Black. Executives like Daniel S. Glaser, who began his career at Marsh in 1982, navigated the same rarified geopolitical circles as Epstein, including the Council on Foreign Relations. This web of influence shielded the network.

Correspondent banking architectures provided the secondary layer of obfuscation. Operating out of WTC 1, Bank of America supplied the channels to move Epstein's offshore capital from the Caribbean into the U.S. system. This allowed tier-one institutions to process illicit liquidity while maintaining a facade of distance. The methodologies used to shield Epstein's capital—offshore shells and blind-basis clearing—descend directly from the structural loopholes of the 9/11 settlement crisis. The opacity designed to protect the Treasury market was repurposed to launder the proceeds of privatized extortion.

This environment was endemic to the pre-9/11 system. A revealing parallel is First Equity Enterprises, a massive currency fraud operating out of the World Trade Center (Gow 2001). After the attacks, managers used the chaos to divert attention from a $100 million shortfall, with funds traced to Swiss accounts. Crucially, First Equity utilized the same banking infrastructure as Epstein—JPMorgan Chase and Bank One. This mirrors Epstein's tenure at Towers Financial Corporation, a Ponzi scheme where he learned corporate obfuscation. Both instances demonstrate how a WTC address and tier-one clearing could mask nine-figure frauds. Notably, no FEE employees were lost in the attack.

WTC North Tower collapses at 10:28am (Posted to Reddit).

The volume of capital sustained this architecture. Epstein directed the wealth of titans like Leslie Wexner and Leon Black. Black paid Epstein an inexplicable \$158 million for tax strategies designed to avoid over \$1 billion in liabilities (Wyden 2023). When executives route personal wealth through a specific advisor, the associated institutions are incentivized to ignore compliance. The prestige of these clients provided the ultimate "compliance shield," forcing risk managers into willful blindness.

The network utilized philanthropy as a sanitized interface. Following 9/11, Edie Lutnick, Howard's sister, co-founded the Cantor Fitzgerald Relief Fund; she was also a "Founding Citizen" of TerraMar, Ghislaine Maxwell's ocean conservation nonprofit. This cover obscured a deeper reality: Epstein's function as a state-sponsored intelligence asset. His network functioned as a "human analog" to the PROMIS software scandal—a mechanism to secure leverage over global command structures. This mirrors the post-9/11 opacity, where charitable vehicles serve as fronts for intelligence integration.

The document release has triggered political consequences. Representative Thomas Massie has called for Lutnick's resignation. This instability is compounded by a scandal involving Lutnick's sons, Brandon and Kyle, who now lead Cantor Fitzgerald (Rashid 2026). Following a Supreme Court ruling striking down tariff policies, allegations surfaced that the Lutnick family used privileged information to bet against the policies their father architected—a next-level insider trading maneuver mirroring the information arbitrage of the post-9/11 era.

VII. Privatizing Covert Economics

The methodologies Jeffrey Epstein utilized to shield his capital descend directly from the structural loopholes engineered during the 9/11 settlement crisis. Offshore shell companies, blind-basis correspondent clearing, and elite compliance overrides constitute the fundamental architecture of the Post-Audit World. The global financial system underwent a permanent structural calibration during moments of profound crisis to accommodate shadow capital. Access to restricted information and elite clearing networks dictates market survival—and the boundaries of legal accountability.

Between late 2001 and 2004, shadow capital networks transitioned this arbitrage strategy from the Treasury market to the broader equity markets. To bypass the reporting mechanisms of the Continuous Net Settlement (CNS) system, these entities utilized "ex-clearing" trades—transactions settled directly between counterparties, often facilitated by prime brokers in lenient jurisdictions like Canada or the Caribbean. By executing massive block trades known as "position rolls" among affiliated offshore entities, hedge funds could reset the regulatory time clock for aged fails, maintaining naked short positions indefinitely while remaining invisible to domestic regulators.

The implementation of Regulation SHO in 2004 codified these crisis-era anomalies into permanent law; the Securities and Exchange Commission successfully privatized the State of Exception. They transformed temporary emergency waivers into specialized financial products. The Grandfather provision (Rule 203(b)(3)(i)) functioned as an unprecedented amnesty program, explicitly shielding older uncollateralized debt from mandatory buy-ins (SEC 2004). This clause allowed the systemic fails generated in the post-9/11 informational vacuum to remain active liabilities forever, permitting offshore hedge funds to maintain massive, un-backed short positions indefinitely without fear of regulatory reprisal (Shapiro 2003, 4).

Simultaneously, the Options Market Maker exception allowed shadow capital networks to outsource the naked shorting mechanics. Market makers exploited this bona fide hedging exemption to build artificially large synthetic short positions, executing naked short sales while maintaining the resulting fails-to-deliver indefinitely (Stratmann and Welborn 2012, 4; SEC 2004). By utilizing synthetic shorts through the options market, they forced market makers—who were statutorily exempt from borrow and locate requirements—to hedge the risk by shorting the underlying stock, legally generating and sustaining massive FTDs (Stratmann and Welborn 2012, 12; Li, Zhao, and Zhong 2015, 11-12). Because the National Securities Clearing Corporation allocates mandatory buy-ins exclusively to the oldest continuous fails, high-volume options market makers effectively immunize themselves from settlement enforcement by rapidly turning over their portfolios (Evans et al. 2006, 4; 29).

The central clearinghouse actively conceals this systemic equity dilution through mathematical obfuscation. Forensic analysis, notably by Dr. Robert J. Shapiro, exposes the fallacy of the National Securities Clearing Corporation's 99 percent settlement claim (Shapiro 2003, 1–4). Shapiro demonstrated that the NSCC's statistics were misleading, underrepresenting the true volume of FTDs by a factor of 25. The fallacy stems from the CNS system, which artificially nets out approximately 96% of gross transaction volume before calculating a final settlement obligation. The 99% success rate applies only to this residual netted balance, burying the massive gross volume of undelivered shares. The clearinghouse operates as a black box for shadow capital. It socializes settlement failures while protecting the prime brokerages generating phantom shares (Shapiro 2003, 4).

The enduring alliance between WTC-legacy figures and shadow financiers demonstrates the true legacy of the 9/11 bond market freeze. The crisis functioned as a macro-financial pivot. It proved that systemic unbacked liabilities could be sustained without penalty. The resulting regulatory dark pools remain the bedrock of modern high finance. Elite interlocks engineered a reality where capital operates entirely exempt from the physical laws of settlement, delivery, and audit. The Lutnick-Epstein files are not an anomaly; they are a user manual for the privatized state.

References

ALI and NCCUSL. 1994. Uniform Commercial Code (UCC) Article 8.

https://www.law.cornell.edu/ucc/8

Craig, Susanne. 2011. "The Survivor Who Saw the Future for Cantor Fitzgerald." The New York Times, September 3.

https://archive.nytimes.com/dealbook.nytimes.com/2011/09/03/the-survivor-who-saw-the-future-for-cantor-fitzgerald/

Department of Justice. 2012. Adfin Solutions, Inc. Series A Preferred Stock Purchase Agreement. Unsealed Epstein Files (Data Set 9). Released January 30, 2026.

https://www.justice.gov/epstein/files/DataSet 9/EFTA00289560.pdf

Dr. Econ. 2000. "Why did the national debt in the hands of the public increase from approximately \$700 billion to over \$2,400 billion during the 1980s?" Federal Reserve Bank of San Francisco, November.

https://www.frbsf.org/research-and-insights/publications/doctor-econ/2000/11/national-debt-80s/

Evans, Richard B., Christopher C. Geczy, David K. Musto, and Adam V. Reed. 2006. "Failure is an Option: Impediments to Short Selling and Options Prices."

https://www.sec.gov/comments/4-520/4520-6.pdf

Federal Deposit Insurance Corporation (FDIC). 1997. History of the Eighties: Lessons for the Future. Vol. 1, An Examination of the Banking Crises of the 1980s and Early 1990s. Washington, DC: FDIC.

https://perma.cc/EZ79-STRH

Financial Markets Law Committee. 2004. "Issue 3 - Property Interests in Investment Securities: Report on research into the 1994 revisions to Article 8 of the Uniform Commercial Code." London: Financial Markets Law Committee.

https://fmlc.org/wp-content/uploads/2018/02/Issue-3-Background-paper-on-Article-8-of-the-Uniform-Commercial-Code.pdf

Fleming, Michael J., and Kenneth D. Garbade. 2002. "When the Back Office Moved to the Front Burner: Settlement Fails in the Treasury Market after 9/11." Federal Reserve Bank of New York Economic Policy Review 8, no. 2: 59–79.

https://www.newyorkfed.org/medialibrary/media/research/epr/02v08n2/0211flempdf.pdf

Gambino, Lauren. 2026. "Democrats accuse DoJ of not releasing millions of Epstein files despite legal requirement." The Guardian, January 31.

https://www.theguardian.com/us-news/2026/jan/31/democrats-justice-department-epstein-files

Goldberg, Alfred, et al. 2007. Pentagon 9/11. Washington, DC: Historical Office, Office of the Secretary of Defense.

https://history.defense.gov/Portals/70/Documents/pentagon/Pentagon9-11.pdf

Government of the United States Virgin Islands. 2023. First Amended Complaint. Government of the United States Virgin Islands v. JPMorgan Chase Bank, N.A., Case No. 22-cv-10904-JSR. U.S. District Court for the Southern District of New York.

https://s.wsj.net/public/resources/documents/usvi-jpm-01-13-2023.pdf

Gow, David. 2001. "$100m fraud probe linked to terror attack." The Guardian, October 26.

https://www.theguardian.com/world/2001/oct/26/september11.usa1

Greene, Connor. 2026. "U.S. Commerce Secretary Faces Calls to Resign Over Epstein Ties." Time Magazine, February 9.

https://time.com/7373253/epstein-files-secretary-howard-lutnick-calls-to-resign/

Heidner, E.P. 2008. Collateral Damage, Part 1.

Ingber, Jeffrey F. 2017. "The Development of the Government Securities Clearing Corporation." Federal Reserve Bank of New York Economic Policy Review (December): 33–50.

https://www.newyorkfed.org/medialibrary/media/research/epr/2017/epr_2017_gscc_ingber.pdf

Kates, Graham. 2026. "Commerce Secretary Howard Lutnick defends visit to Epstein's island with his family." CBS News, February 10.

https://www.cbsnews.com/news/howard-lutnick-jeffrey-epstein-island-visit/

Lacker, Jeffrey M. 2003. "Payment System Disruptions and the Federal Reserve Following September 11, 2001." Working Paper 03-16. Federal Reserve Bank of Richmond.

https://www.richmondfed.org/-/media/richmondfedorg/publications/research/working_papers/2003/pdf/wp03-16.pdf

Langley, Monica. 2003. "Into the WASP Nest," In Tearing Down the Walls: How Sandy Weill Fought His Way to the Top of the Financial World... and Then Nearly Lost It All. New York: Simon & Schuster.

Li, Yubin, Chen Zhao, and Zhaodong (Ken) Zhong. 2015. "Migrate or Not? The Effects of Regulation SHO on Options Trading Activities."

https://acfr.aut.ac.nz/__data/assets/pdf_file/0008/29717/C-Zhao-A.3.3-SHO-paper.pdf

McAndrews, James J., and Simon M. Potter. 2002. "Liquidity Effects of the Events of September 11, 2001." FRBNY Economic Policy Review 8, no. 2 (November): 59–79.

https://www.newyorkfed.org/medialibrary/media/research/epr/02v08n2/0211mcanpdf.pdf

National Commission on Terrorist Attacks Upon the United States. 2004. The 9/11 Commission Report. Washington, DC.

https://www.9-11commission.gov/report/911Report.pdf

Poteshman, Allen M. 2006. "Unusual Option Market Activity and the Terrorist Attacks of September 11, 2001." The Journal of Business 79, no. 4: 1703–1726.

https://www.jstor.org/stable/10.1086/503645

Rashid, Hafiz. 2026. "Trump Secretary Silent as Sons Poised to Make Bank From End of Tariffs." Yahoo Finance.

https://finance.yahoo.com/news/trump-secretary-silent-sons-poised-213852683.html

Ruetenik, Daniel, and Graham Kates. 2026. "Lutnick and Epstein were in business together, Epstein files show." CBS News, February 7.

https://www.cbsnews.com/news/howard-lutnick-jeffrey-epstein-in-business-together/

Scheider, Fabienne. 2025. "On-the-run Premia, Settlement Fails, and Central Bank Access." Bank of Canada Staff Working Paper 2025-19.

https://www.bankofcanada.ca/wp-content/uploads/2025/08/swp2025-19.pdf

Scott, Peter Dale. 2007. The Road to 9/11: Wealth, Empire, and the Future of America. Berkeley: University of California Press.

Shapiro, Robert J. 2003. "Comments on the 'Proposed Rule: Short Sales,' 17 CFR 240 and 242, Release No. 34-48709." Securities and Exchange Commission, File No. S7-23-03.

https://www.sec.gov/rules/proposed/s72303/rshapiro122403.htm

Stratmann, Thomas, and John W. Welborn. 2012. "The Options Market Maker Exception to SEC Regulation SHO." Working Paper, Mercatus Center, George Mason University (August): 1–46.

https://www.mercatus.org/sites/default/files/d7/stratmann-wp-v1.01-copy.pdf

U.S. Securities and Exchange Commission. 2001. Emergency Order Pursuant to Section 12(k)(2) of the Securities Exchange Act of 1934. Release No. 44791, September 14.

https://www.sec.gov/rules-regulations/2001/09/emergency-order-pursuant-section-12k2-securities-exchange-act-1934-taking-temporary-action-respond

U.S. Securities and Exchange Commission. 2004. Short Sales. Final Rule. Release No. 34-50103. 69 FR 48008.

https://www.sec.gov/rules-regulations/2004/07/short-sales

U.S. Senate. 2021. Waste, Fraud, Cost Overruns, and Auditing at the Pentagon. Committee on the Budget. 117th Cong., 1st sess., May 12. S. Hrg. 117-46.

https://www.govinfo.gov/content/pkg/CHRG-117shrg45251/html/CHRG-117shrg45251.htm

Wyden, Ron. 2023. "Wyden Unveils Ongoing Investigation Into Private Equity Billionaire Leon Black's Tax Planning and Financial Ties with Jeffrey Epstein." United States Senate Finance Committee, July 25.

https://www.finance.senate.gov/chairmans-news/wyden-unveils-ongoing-investigation-into-private-equity-billionaire-leon-blacks-tax-planning-and-financial-ties-with-jeffrey-epstein

Zarembka, Paul, ed. 2008. The Hidden History of 9/11. New York: Seven Stories Press.